I would like to anchor my story around a Japanese regulation you might not be familiar with. When a construction site is active in Japan, contractors are required to measure noise pollution. Generally, these regulations aim to keep noise under 85 dB(A), and for this constant monitoring is necessary, which is often done using calibrated noise meters around the perimeter of the construction site. In some cases, vibration levels may also need to be monitored. For those familiar with Japan, it comes as no surprise that there is a strong emphasis on quietness throughout society, particularly at some venues. This is where RION CO., LTD (TSE: 6823) offers the necessary products to fulfill the various noise regulation laws, among other product segments, for which demand has been increasing over the past years (more on this later).

A Flashback: 80 Years of Innovation

In the early days, before the company was named RION, which is a combination of Rigaku (理学) and Onkyogaku (音響学) – the fields of science and acoustics, it was part of Kobayashi-Riken Institute. The company was established to commercialize the research results into a viable product, mainly centered around environmental noise and vibration. After World War II ended and Japan was rebuilding itself, there was a considerable amount of environmental challenges, which RION and various government agencies addressed in part by products developed by Rion.

Up until the 1980s their products were focused on Sound Level Meters and Vibration Meters, but this changed with the introductions of various world’s firsts in the following years:

- The world’s first hearing instrument with Automatic Noise Suppression (ANS).

- The world’s first 1/N Realtime Analyzer.

- The world’s first cartilage conduction hearing instrument

Throughout their 80-year history, their philosophy has been anchored in contributing to society through advancements in science and technology. And this is also reflected in their current product groups:

- Hearing Instruments: Capitalizing on the “silver economy” by providing advanced hearing solutions for Japan’s rapidly aging society.

- Medical Equipment: Supplying essential diagnostic tools, such as audiometers, that form the backbone of ENT (Ear, Nose, and Throat) clinics nationwide.

- Sound & Vibration Measuring Instruments: A stable moat through regulatory compliance, providing the precise tools required by law for construction and industrial noise monitoring, and other environmental measurements (ESG).

Particle Counters: Critical contamination control technology for the high-precision semiconductor and pharmaceutical manufacturing sectors.

Breaking down their Business

In the financial reporting, Rion simplifies the previously mentioned products into three business segments, in which Hearing Instruments are included within Medical Instruments.

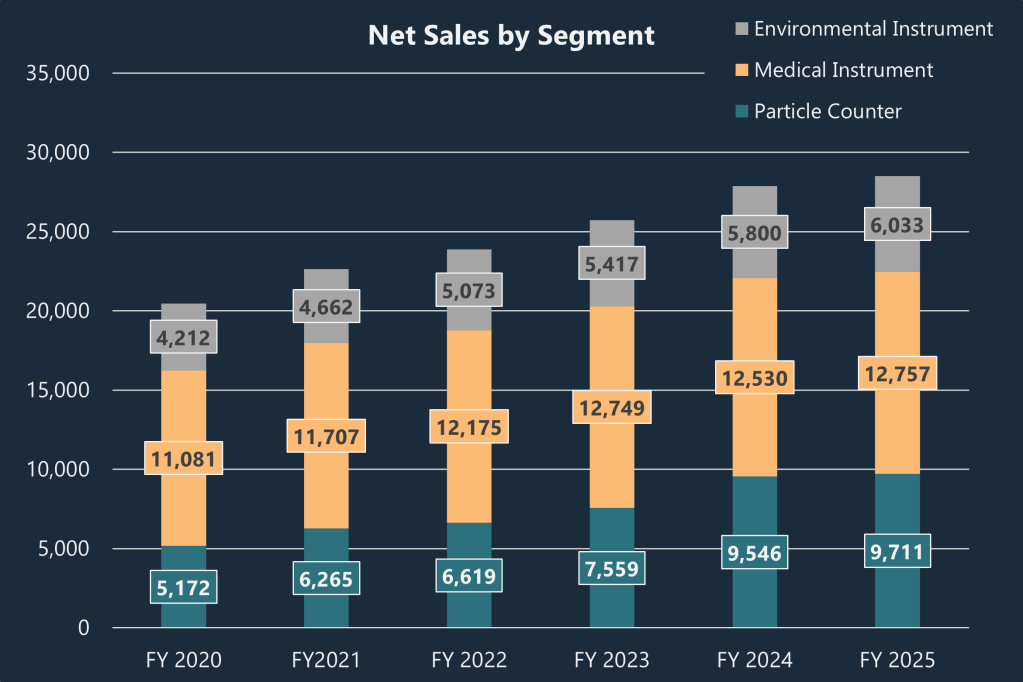

Starting with the top line there is a steady increase in revenue since FY 2020, averaging around 7.2% in annual growth (CAGR), however when looking at the different business segments, it becomes clear that the main growth driver has been Particle Counters followed by the Environmental Instruments.

Despite Medical Instruments making up the biggest portion of the revenue share, its growth has been stagnant, and could take the second position after the Particle Counters, if its growth remains steady. While at the beginning of this write-up, I shared an insight about the Japanese construction industry, you might have been led to believe that the Environmental Instruments were their main business/growth driver. However, it seems like they have been able to cross-engineer, and utilize their existing know-how in a separate field that has seen unprecedented demand: AI.

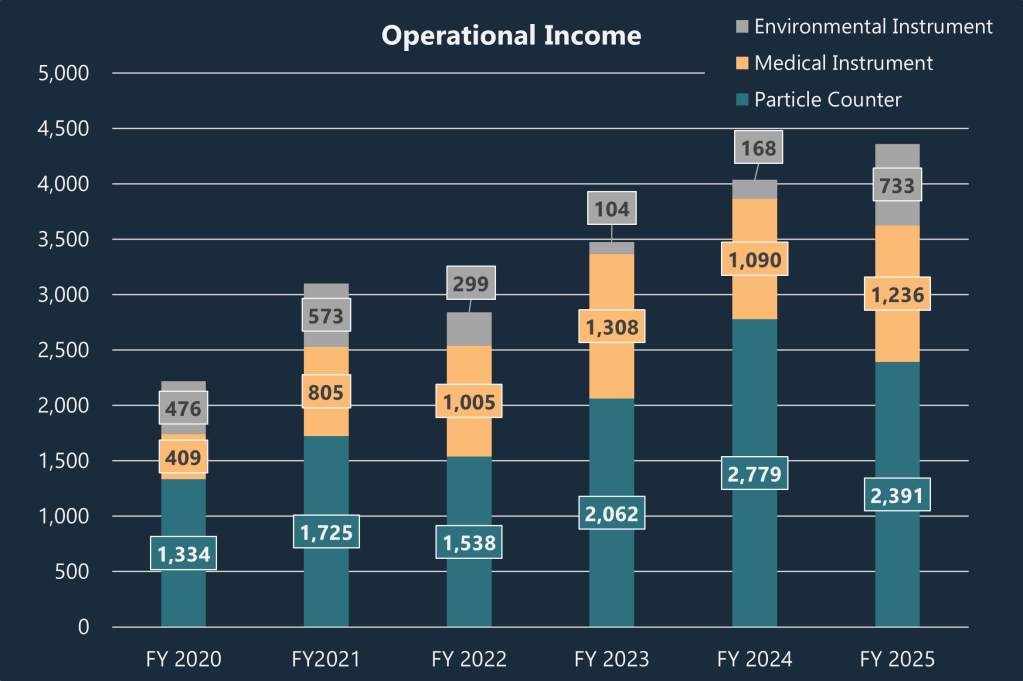

To get a better picture of the various contributions the different business segments are delivering, I would like to show you the breakdown of the operational incomes, which shows a considerable amount of income being generated by the Particle Counter business.

Particle Counter Division

The income growth is in line with the top-line, however despite the revenue reaching a record high in FY 2025, the income generated from the Particle Counter business decreased by around 14% compared to the previous financial year. From the earnings calls, they are giving two reasons for this:

- Spending on Increasing Production Capabilities

- Spending on Additional R&D Costs

This tells me that in previous corporate planning rounds, they had not foreseen the growth that would come with the AI build-out and how they could prepare themselves to quickly scale their business to meet the market demand.

The decline in income highlights that they have reached their operational capacity. While this in itself is not necessarily bad, it is crucial that they ramp up the production in line with future market demand, and avoid the situation where additional capacity was ensured, while the market situation has changed or vice versa; especially for expansion periods in the future.

Although I lack direct proof, I would like to propose a constructive perspective on the rise in R&D expenditure. It is my view that RION’s semiconductor clients follow specific roadmaps for their current and upcoming technical needs. To capture greater market share, RION must likely enhance the technical specifications of its offerings, especially as the semiconductor sector’s shift toward smaller scales demands increasingly rigorous precision throughout the fabrication workflow. Consequently, this growth in R&D investment underscores a confident and favorable outlook for the Particle Counter unit.

Coupling this with the ramp-up of the production capabilities, there is a strong indication for further growth in the near-term future.

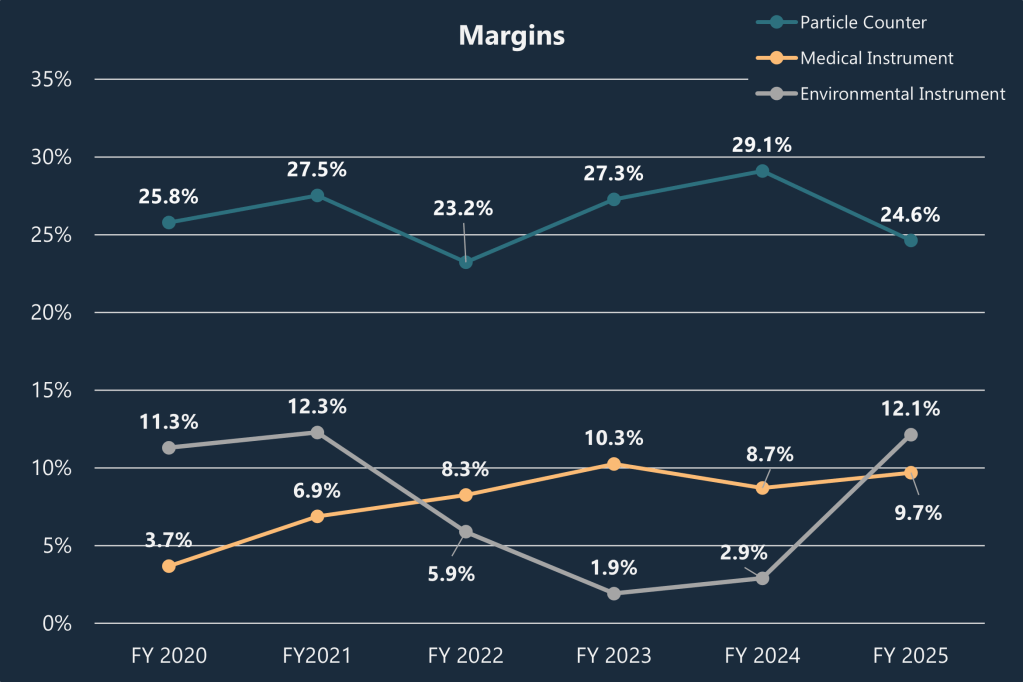

Before we move onto the next business division, I think it is necessary to show just how profitable the Particle Counter division is compared to the Medical Instruments and the Environmental Instruments. Over the last five financial years (FY), RION has consistently achieved margins of 23% or more, reaching nearly 30% in FY 2024. This means, around 54% of the earnings in FY 2025 were generated in the Particle Counter division.

These results clearly speak for a strong product foundation (i.e. good quality products) coupled with a strong market demand. It will be crucial for RION to keep these exceptional margins steady while they ramp-up production, to defend and grow their market share.

Regarding the competitive landscape in this sector, the primary rival is Particle Measuring Systems (PMS/Spectris), the current market leader that commands roughly one-third of the $630 million industry.

While PMS operates as a global leader with a broad product suite, Rion’s $62 million in divisional revenue is strategically anchored by its expertise in high-sensitivity instrumentation for the semiconductor supply chain, particularly within the Asian market. Rion maintains its competitive standing alongside other significant players, such as Danaher’s Beckman Coulter and specialized firms like TSI Incorporated and Lighthouse Worldwide Solutions.

Medical Instrument Division

While the top-line of the Medical Instrument business has only grown marginally (+15% over 5 years), the operational income has shown a much more favorable development, which clearly outpaces the top-line numbers: The operational income has tripled, from 409 million yen to 1,236 million yen, and translates into a margin improvement from a meager 3.7% to around 10%.

Based on the historical financial data and future outlooks provided from 2022 to 2026, Rion’s Medical Instruments division (which includes hearing aids and medical equipment) focused on a combination of high-value product innovation, strategic partnerships, and operational efficiency to drive earnings. While the division faced a temporary dip in 2025, the overall historical trend of increasing profitability was driven by the following factors (based on the earning release documents in Japanese):

- Shift towards High-Value-Added Products: The most significant driver of margin expansion was the introduction and promotion of high-margin products, specifically through the launch of the “Rionet 2” series. By prioritizing sophisticated, upper tier models, they successfully increased the average sales price per unit.

- Enhancing existing Sales Channels: Rion is strategically utilizing its clinical reputation by using medical equipment sales as a foothold in ENT clinics. This creates an exclusive access to patients who are otherwise inaccessible via traditional retail channels.

- Strategic Price Adjustments: To combat the rising costs of raw materials and energy, Rion implemented a policy of sales price adjustments across its segments. By passing on some of the increased component costs to the market, they were able to protect their margins.

- Operating Leverage and Scaling: Better earnings performance through fixed cost absorption. Furthermore, Rion integrated manufacturing subsidiaries (merging Rion Techno and Rion Metal Industry in 2023) to streamline manufacturing operations and improve overall business efficiency.

The aforementioned factors certainly catalyzed margin expansion; however, the broader margin trends and revenue figures indicate a challenging market environment, primarily because the product portfolio has reached a state of maturity. On the positive side, however, this sector is less likely to experience a volatile market landscape, providing a dependable foundation for consistent revenue. Future profitability increases will likely stem from continued optimization of operating leverage and the execution of strategic pricing measures.

In the Medical Instruments division, Rion maintains a commanding domestic position as Japan’s leading hearing aid provider through its “Rionet” brand. While the global audiology market is dominated by a concentrated group of international leaders: such as Sonova, Demant, WS Audiology, GN Store Nord, and Starkey; Rion’s competitive edge is anchored in its extensive nationwide network and deep integration into the Japanese clinical infrastructure.

Domestically, the company faces competition from diversified electronics giants such as Panasonic and Omron, as well as specialized players like Nikon-Essilor. Despite the relative maturity of the Japanese market, Rion has sustained its leadership by shifting toward high-value digital hearing solutions and audiometers, leveraging Japan’s aging demographic to transform a legacy business into a consistent and stable source of cash flow.

Environmental Instruments Division

Finally, I want to discuss the Environmental Instruments unit. While this division has historically provided the smallest portion of total revenue, it has achieved a compound annual growth rate of approximately 7.4% over the past five years. Interestingly, this top-line expansion has not improved the bottom line; in fact, profitability has declined, with margins hitting a precarious 1.9% in FY 2023.

Understanding RION’s transition requires a look at the catalysts behind their shift. Financial data from 2022 to 2026 reveals that the Environmental Instruments unit experienced a major overhaul. What was once a primarily domestic operation became a globally integrated entity following the total acquisition of Norsonic AS in 2022, a prominent Norwegian producer of sound measurement technology. The resulting acquisition and integration costs shrunk the margins significantly.

This strategic move served as a pivotal moment for the sector, intended to bolster RION’s international presence and secure access to “NorCloud,” Norsonic’s sophisticated environmental monitoring platform.

You can think of NorCloud as a proprietary, subscription-based command center that automates remote noise monitoring and data collection exclusively for Norsonic hardware. It trades manual labor for recurring operational efficiency, effectively locking you into a high-precision, but closed ecosystem.

This goes hand-in-hand with their overall corporate strategy to expand the product portfolio from handheld devices to monitoring solutions on large scale systems, such as noise level monitoring at airports. Furthermore, unlocking new clients in the European market, and securing a global footprint.

In the following years you can see a healthy recovery of the margins to the previous high levels of around 12%. Though it remains premature to gauge the complete impact of their synergies, this move represents a clear stride toward business expansion, and as the saying suggests, fortune favors the bold.

Its primary international rival is Hottinger Brüel & Kjær (HBK), which commands a significantly larger global share. Through the acquisition of Norway’s Norsonic AS, Rion is directly taking on European specialists like SVANTEK and Casella. While Rion leads domestically against rivals like Ono Sokki, its international growth hinges on whether its specialized focus on regulated noise environments can effectively penetrate markets long-held by established Western conglomerates.

A Diversified Business with Growth Ambitions

While Rion’s current financial reports do not provide a breakdown of revenue by geographical region, their strategic acquisition of Norsonic AS clearly signals an ambition to expand beyond the domestic Japanese market. A similar international focus is evident in the Particle Counter division, which supplies products to manufacturing sites on a global scale. I believe both divisions will serve as key growth drivers, supported by robust market demand that should sustain their positions in the coming years.

Conversely, the Medical Instruments division represents the company’s established core. Although its growth potential is capped by the maturity of the Japanese market, it remains a reliable source of revenue, protected by a significant competitive moat built on its extensive nationwide medical network.

To summarize, Rion’s diversified corporate architecture places it in a strong strategic position, combining the stability of established sectors with significant participation in high-growth markets. Although the Medical Instruments division is sometimes viewed as a legacy unit with restricted growth prospects, it provides a vital safety net during economic downturns when corporate capital expenditures tighten, offering resilience to navigate challenging periods.

About the Financials

At the time of writing the stock is trading at around 3,620 Yen. With a market capitalization of approximately 45 billion Yen (around 287 million USD), with a P/E of 13.5x

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or professional advice. While the data presented is based on public earnings reports and market analysis available as of May 2026, market conditions can change rapidly. The author holds no responsibility for any financial losses resulting from the use of this information. Always conduct your own due diligence or consult with a certified financial advisor before making investment decisions.

Leave a comment