For years, Japanese companies have been criticized for being a bit stuck in their ways: Clinging to old cross-shareholdings and dragging their feet on selling off tired businesses. But things are changing. Noritsu Koki Co., Ltd. (TSE: 7744) is a perfect example of this new wave. They’ve pulled off a major pivot, moving from a struggling analog manufacturing past into a smart, global holding company. Today, they own a portfolio of highly profitable, niche-leading businesses. Let’s dive into Noritsu Koki’s business model, what they actually own, how they handle currency swings, and why they might be a great long-term “compounder” for regular investors.

How the Holding Strategy Came to Life

From Photo Labs to Digital Prowess

Starting out in Wakayama back in 1951, Noritsu Koki made its name with top-tier photo gear. They launched the world’s first automated monochrome film processor in 1961 and the game-changing QSS-1 minilab in 1976. These inventions meant stores could develop and print film right on the spot. It was a huge hit, fueling massive growth across the globe, especially in North America, and eventually leading to their stock market debut in 1997.

But when digital photography took over in the mid-2000s, the traditional photo market took a permanent nosedive. Noritsu had to make some tough calls. After a big shake-up in 2008, they set up NK Relations in 2009 to move beyond their fading imaging business. By 2011, they’d transitioned into a pure holding company and started a busy streak of buying up companies in everything from healthcare and senior living to agriculture and materials science.

When CEO Ryukichi Iwakiri took the reins in 2018, he started cleaning house. He sold off mature or “non-core” pieces like direct healthcare and senior mail-order businesses. They even stepped away from making photo hardware in 2016, though they later brought the “Noritsu Precision” brand back into the fold in 2021. Today, Noritsu is a focused holding company that manages subsidiaries dominating very specific, specialized niches.

The “Serial Acquirer” Playbook

Noritsu’s playbook revolves around a simple vision: “No. 1/Only 1.” Basically, they only want to own businesses that are leaders in their field with high barriers to entry. They aren’t just looking for corporate synergy; they act like a programmatic compounder. They take the cash flowing from their established companies and use it to buy new, asset-light, and highly profitable targets.

This approach puts them in a special club of serial acquirers. In Japan, where many successful small businesses are looking for someone to take over as owners retire, Noritsu’s model is becoming a vital part of the country’s corporate evolution.

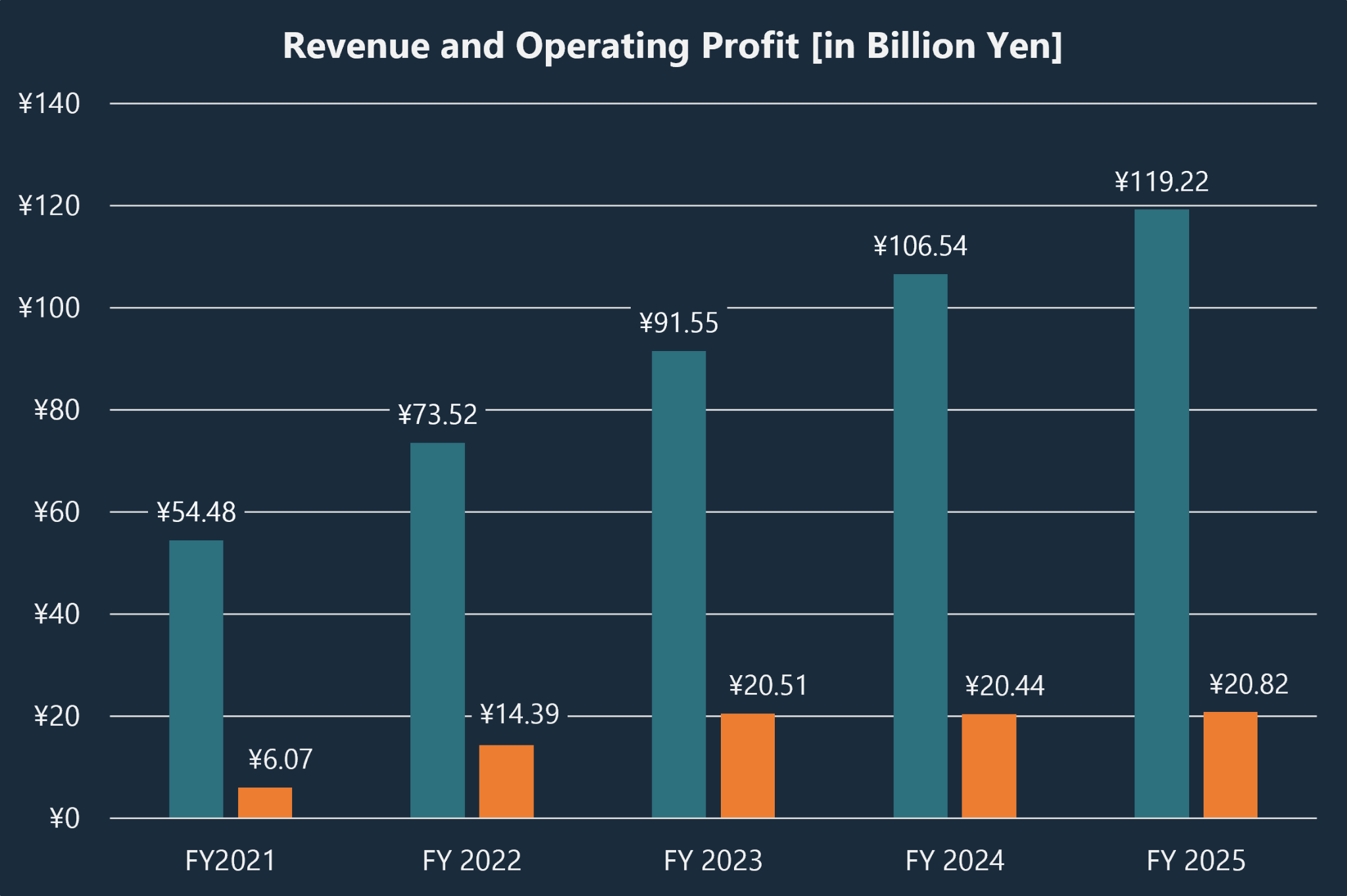

The steady growth of Noritsu is visible in their revenue which has grown from around 54 billion yen to nearly 120 billion yen in just 4 years, which averages to around 21.6% growth per year.

Are They the Berkshire Hathaway of Japan?

Comparing Noritsu to Berkshire Hathaway shows some cool similarities and some big differences. Operationally, both love a decentralized setup. Noritsu’s lean headquarters lets the subsidiary leaders call the shots on daily business, products, and customers. This keeps things fast and focused, while the parent company handles the big-picture stuff like where to put capital and how to manage the treasury.

But the way they get their money is totally different:

- The Cash Engine: Berkshire has its famous “float” from insurance. Noritsu doesn’t. Instead, they fund deals with cash from their subsidiaries, profits from selling off older assets, and low-interest bank debt from Japan. They often use yen loans (like they did for their most recent big purchase) to lock in new acquisitions.

- Holding vs. Selling: While Warren Buffett famously likes to hold “forever,” Noritsu is more active. They’re happy to sell a business once it matures if they can get a great price and reinvest that money into something with even better growth potential.

Meet the Portfolio: What Noritsu Actually Does

Noritsu’s current lineup is built around two main pillars: Audio Equipment, Parts & Materials, including their newest addition to the construction world: SENQCIA.

1. Teibow Holdings (The Backbone of Every Pen)

Noritsu bought Teibow in 2015, but the company has been around since 1896! They are the unsung heroes of the stationery world. (https://teibow.co.jp/english/business/)

- Market Muscle: They own about 50% of the global market for pen nibs made of felt and fiber. To keep growing, they just spun off a new tech division called Hamamatsu Metal Works in early 2025 to focus on specialized metal parts.

- The Silent Partner: Since they sell to other businesses, you won’t find them on Yelp. But in the pen world, they are legendary. Once a manufacturer picks a Teibow nib, it’s hard to switch because it affects the whole ink chemistry. That gives Teibow incredible “stickiness” with their customers.

- Recent Numbers: Revenue dipped slightly in 2025 due to customers clearing out old inventory and rising costs, but they’ve already started bouncing back in early 2026.

- What’s Next: The big bet is on Metal Injection Molding (MIM). It lets them make complex metal parts for medical robots and cars, opening up a whole new world of growth beyond pens.

2. AlphaTheta (The Heart of Global DJ Culture)

AlphaTheta (you probably know them as Pioneer DJ) joined the group in 2020. They are a profit-making machine. (https://alphatheta.com/en/company/)

- Dominating the Booth: They own about 70% of the professional DJ market. From the mixers in the club to the software DJs use at home, they are the industry standard.

- What DJs Say: Pro DJs love the new XDJ-AZ system, giving it nearly perfect 5-star reviews. They love the touchscreens and the fact that you can stream tracks directly from Tidal. It feels just like the top-tier gear you find in world-class clubs.

- Financial Beat: The business is booming. Revenue jumped over 11% in 2025 and exploded even higher in early 2026, thanks in part to some favorable currency swings.

- Growth Remix: They are moving into subscription software and cloud services, ensuring they stay at the cutting edge of how music is played and managed.

3. JLab (Quality Sound for Everyone)

Bought in 2021 for $370 million, JLab is California’s gift to budget-conscious music lovers. (https://www.jlab.com/)

- Value Leader: They are the #1 seller of wireless earbuds under $100 and headphones under $50 in the U.S. They’ve nailed the “bang for your buck” sweet spot.

- Consumer Choice: People love them. Products like the JBuds Mini get high marks for being compact, durable, and having a great app. They’re the go-to for daily workouts and office calls without breaking the bank.

- Recent Performance: Revenue grew nicely in 2025, but they hit a speed bump in early 2026 due to new U.S. tariffs and some inventory write-downs. It’s a temporary dip as they transition to new products.

- Global Reach: Noritsu is now helping JLab expand across Europe and Asia, while the brand starts launching higher-end “Pro” models to capture more of the market.

4. SENQCIA (Making Buildings Safer)

In early 2026, Noritsu made its biggest move yet: buying SENQCIA for about ¥69 billion. It’s a massive addition to the family.

- Construction Core: They provide the floors for data centers and cleanrooms, plus high-tech systems that help buildings withstand earthquakes.

- Trusted Name: With 60 years under their belt, they are a staple in Japanese construction. Their specialized floors are essential for heavy semiconductor gear, and their earthquake reinforcement can be installed without even closing the building down. That’s a huge win for landlords.

- Financial Impact: SENQCIA is already a heavy hitter, bringing in billions in revenue. They are a significant new driver for Noritsu’s overall profits.

- Building the Future: As more data centers pop up for AI and more semiconductor factories are built, SENQCIA is perfectly placed to grow right along with them.

Dealing with the Yen: How Currency Matters

Since more than 90% of their money comes from outside Japan, the value of the Japanese yen is a huge deal for Noritsu.

USD/EUR earnings appreciation:

| Conversion Gains | Overseas Production Cost |

| – Revenue up 48.2% YoY – OP up 60.5% YoY | – Material costs rise in JPY – Margins compressed locally |

A Balancing Act

Currency swings hit them in two ways:

- The Bonus: When the yen is weak, every dollar or euro they earn abroad is worth more yen when they bring it home. This helped boost their reported profits significantly in early 2026.

- The Cost: On the flip side, a weak yen makes it more expensive to import materials for their Japanese factories. It’s a give-and-take.

Natural Defense

Instead of buying expensive financial protection, Noritsu uses a “natural hedge.” They try to match their foreign income with their foreign debt and expenses. By keeping it all in the same currency locally, they stay more stable when the markets get wild.

Net Currency Exposure= (Foreign Revenue-Foreign Op. Exp.)-Foreign Debt Service

By funding overseas acquisitions with foreign-currency debt and using local manufacturing facilities, the company matches its incoming cash flows with its debt and tax obligations. This operational alignment helps stabilize cash flows and reduces transaction-related currency risks.

Checking the Books: Debt and Value

All those deals have changed Noritsu’s balance sheet, adding some new debt and intangible assets.

The Post-SENQCIA World

Buying SENQCIA in early 2026 made the company’s asset list grow quite a bit. Here’s a quick look at how the numbers shifted after the deal:

| Balance Sheet Line Item (IFRS, ¥ Millions) | December 31, 2025 | March 31, 2026 | Absolute Change | Percentage Change |

| Cash and Cash Equivalents | 97,399 | 64,597 | -32,802 | -33.7% |

| Trade and Other Receivables | 16,871 | 23,793 | +6,922 | +41.0% |

| Inventories | 23,701 | 27,393 | +3,692 | +15.6% |

| Goodwill | 50,333 | 114,921 | +64,588 | +128.3% |

| Intangible Assets | 73,697 | 86,037 | +12,340 | +16.7% |

| Other Non-Current Assets | 12,208 | 15,514 | +3,306 | +27.1% |

| Total Assets | 301,798 | 363,688 | +61,890 | +20.5% |

| Current Liabilities | 39,220 | 55,455 | +16,235 | +41.4% |

| Non-Current Liabilities | 33,987 | 79,642 | +45,655 | +134.3% |

| Total Liabilities | 73,324 | 135,098 | +61,774 | +84.2% |

| Total Equity | 228,474 | 228,590 | +116 | +0.1% |

The Risk of “Goodwill”

Because they bought SENQCIA for more than just its physical parts, Noritsu added about ¥64.6 billion in “goodwill” to the books. Now, more than half of their total assets are things like brand value and intellectual property rather than physical machines or buildings.

Goodwill-to-Assets Ration = GoodwillTotal Assets

When combined with ¥86,037 million in capitalized intangible assets, non-physical premium assets represent 55.3% of Noritsu Koki’s total asset base.

This is standard, but it means if one of their companies starts to struggle, Noritsu might have to take a “write-down” on that value. It wouldn’t cost them actual cash, but it would make their reported profits and total equity look smaller on paper. It’s something to watch during their annual checks.

Financing the Growth

They paid for SENQCIA with ¥30 billion in cash and ¥50 billion in new debt. This move took them from having more cash than debt to being a more “leveraged” company. They’re now using their credit to fuel that expansion.

Luckily, their businesses make a lot of cash, so they’re well-equipped to pay off those loans. But it does mean they’ll be more focused on paying down debt for a bit rather than jumping into another massive acquisition right away.

Wrapping It Up: The Investment View

Deciding to invest in Noritsu means weighing their exciting growth against the usual risks of a busy holding company.

A Value Disconnect?

Right now, Noritsu looks a bit undervalued compared to similar companies. It’s trading at a lower P/E and P/B ratio than its peers.

This “conglomerate discount” happens when investors find a company a bit too complex to value easily. But if Noritsu keeps hitting its targets for the next few years—aiming for 10% growth and strong margins—the market might finally give them the credit they deserve.

Here’s a snapshot of the main numbers and targets to keep an eye on:

| Investment & Operating Metric | FY24 Historical | FY25 Actual | FY26 Consolidated Forecast | MTMP FY30 Targets |

| Consolidated Revenue | ¥106,539 million | ¥119,223 million | ¥167,600 million | ¥190,000 million+ |

| Operating EBITDA | ¥24,283 million | ¥25,726 million | ¥35,500 million | ¥38,000 million+ |

| Operating Profit Margin | 18.7% | 17.5% | 15.5% | 15.0% or more |

| Net Profit | ¥16,120 million | ¥15,639 million | ¥16,800 million | — |

| Basic Earnings Per Share | ¥150.54 | ¥146.95 | ¥156.43 | — |

| Annual Dividend Per Share | ¥181.00 | ¥73.67 (Split-Adjusted) | ¥75.00 | 3.5% DOE Floor |

| Total Shareholder Return Ratio | 40.2% | 63.0% | 66.0% | 50.0% or more |

| Consolidated ROE | 7.5% | 6.9% | 7.3% | 10.0% or more |

Keeping Shareholders Happy

Noritsu is very generous with its dividends. For 2026, they’ve proposed a healthy payout of ¥75.00 per share. Their policy is to pay out at least 40% of their earnings, and they’ve even set a “floor” for dividends to make sure they stay stable even if earnings have a rough year.

Plus, they do share buybacks. Overall, they are very focused on making sure shareholders get a piece of the pie. Their solid finances mean they can afford to keep this up while still paying down their new debt.

Risks to Keep on Your Radar

Even with a great track record, there are things to watch out for:

- Intangible Value: A big chunk of their value isn’t “physical,” so any hit to a major brand like JLab or SENQCIA could force them to lower their reported asset values.

- Debt Management: Managing that ¥50 billion in new debt will take a steady hand and consistent cash flow from their businesses.

- Global Policy: Changes in trade deals or tariffs—especially for electronics—could put a squeeze on their profit margins abroad.

The Big Picture

In short, Noritsu Koki is a worthwhile find in Japan: a smart capital allocator that’s rebuilt itself for the modern world. By letting its niche-leading businesses run themselves and focusing on growth, it’s become a powerful engine for long-term value. With steady dividends and a clear plan for the future, Noritsu is a compelling option for anyone looking to invest in the new face of corporate Japan.

Disclaimer: This article is for informational and educational purposes only and does not constitute financial, investment, or professional advice. While the data presented is based on public earnings reports and market analysis available as of June 2026, market conditions can change rapidly. The author holds no responsibility for any financial losses resulting from the use of this information. Always conduct your own due diligence or consult with a certified financial advisor before making investment decisions.

Leave a comment